While we mentioned in the loan facts section of this website that the minimum HUD 221(d)(4) loan is $2 million, and there is no upper limit, the reality can be a little bit more complex. While there technically is no financial ceiling for the program, particularly large loans are typically subject to stricter requirements, especially those involving DSCR and LTC.

Loan Requirements for Very Large HUD 221(d)(4) Loans

While we mentioned in the loan facts section of this website that the minimum HUD 221(d)(4) loan is $4 million, and there is no upper limit, the reality can be a little bit more complex. While there is technically no financial ceiling for the program, particularly large loans are typically subject to stricter requirements, especially those involving DSCR and LTC.

LTC and DSCR Limits for Larger HUD Multifamily Construction Loans

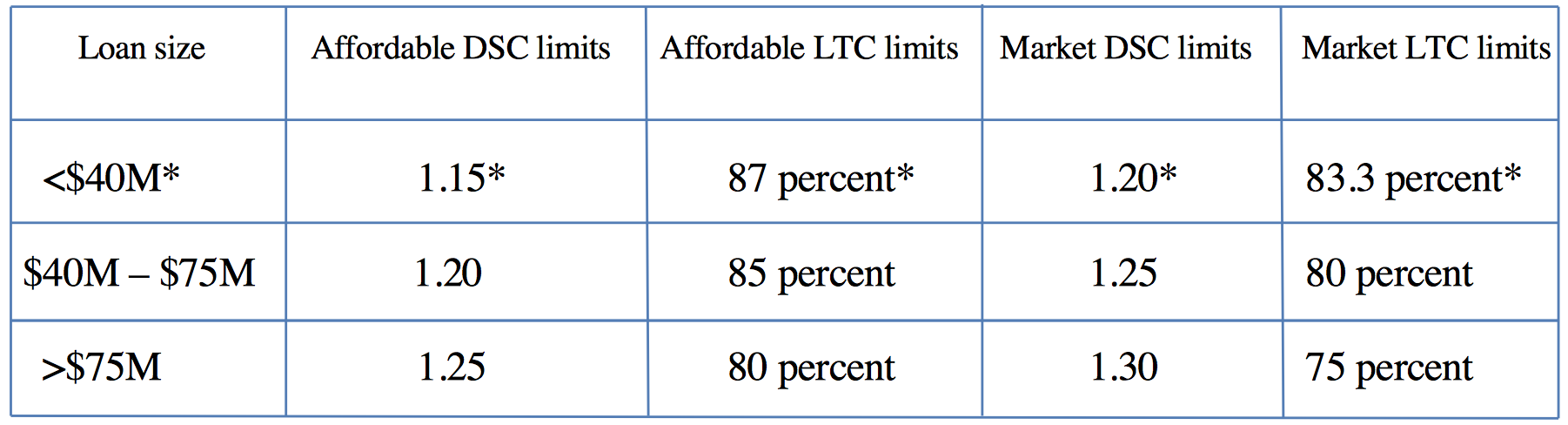

For HUD multifamily construction loans larger than $40 million:

The affordable DSCR limit is 1.15

The affordable LTC limit is 87%

The market DSCR limit is 1.20

The market LTC limit is 83.3%

For loans between $40- $70 million:

The affordable DSCR limit is 1.20

The affordable LTC limit is 85%

The market DSCR limit is 1.25

The market LTC limit is 80%

For loans between $75- $100 million:

The affordable DSCR limit is 1.25

The affordable LTC limit is 85%

The market DSCR limit is 1.30

The market LTC limit is 75%

This information is also shown in the table below, and is taken directly from the HUD website:

HUD 221(d)(4) Loans Larger Than $100 Million

For HUD multifamily construction loans larger than $100 million, special LTC, LTV, and DSCR requirements may apply. This is due to the additional risk that HUD/FHA is taking on by insuring a loan of this size.

To learn more about HUD 221(d)(4) loan limits and requirements, get a financing quote and a HUD loan advisor will get in touch.

Related Questions

What are the benefits of a HUD 221(d)(4) loan?

The HUD 221(d)(4) loan program offers an incredible opportunity for multifamily investors and developers to access the industry’s longest-term form of fixed-rate construction and substantial rehabilitation financing. With terms of up to 40 years (43 years with the 3-year construction period), these loans are also non-recourse, fully assumable, and offer high leverage.

In general, it’s extremely difficult for investors and developers to find financing that will cover both the construction and post-construction period for a multifamily property, all in one loan. This is especially the case since Fannie Mae and Freddie Mac do not provide financing for the construction of multifamily properties, only for property rehab, acquisition, and refinancing (and certain combinations thereof).

In most cases, multifamily investors and developers will have to take out an more expensive bank loan, which will only permit up to 75% LTC in most cases. After, they’ll need to refinance into a permanent loan, which will often come in the form of CMBS financing, Freddie Mac, Fannie Mae, or even a HUD multifamily refinancing loan, such as the HUD 223(f) loan.

Having to deal multiple closings can be expensive, as appraisals, third-party reports, legal, and other costs will be repeated twice in the span of a year or two. However, with a HUD 221(d)(4) loan, investors and developers can access the same long-term, fixed-rate financing for both the construction and post-construction period, all in one loan.

What types of projects are eligible for a HUD 221(d)(4) loan?

HUD 221(d)(4) financing is available for a broad spectrum of developments, including market-rate, low-to-moderate income, and subsidized multifamily, cooperative housing, and affordable housing properties with at least five units. Eligible properties include detached, semi-detached, walkup, row, and elevator-type multifamily properties. For more information, please see HUD 221(d)(4) Construction & Rehab Loans.

What are the requirements for a HUD 221(d)(4) loan?

The requirements for a HUD 221(d)(4) loan include a full scope of third party reports (environmental assessment, market study, appraisal, etc.), annual review, a bonded and licensed general contractor, and compliance with Davis Bacon wage requirements. Additionally, borrowers must have a maximum LTV of 85% for market-rate properties, 87% for affordable properties, and 90% for properties with 90% or more low-income units. A bonded, licensed, and insured general contractor must also execute a GMP contract.

What is the maximum loan amount for a HUD 221(d)(4) loan?

The maximum loan amount for a HUD 221(d)(4) loan is not limited. According to Apartment Loans, the minimum loan amount is $4 million, but exceptions are made on a case-by-case basis. Generally, most 221(d)(4) construction loans are $10 million and above. There is no maximum loan amount.

What is the interest rate for a HUD 221(d)(4) loan?

Interest rates for HUD 221(d)(4) loans are fixed throughout the life of the loan (both construction and permanent stages) and determined at commitment by prevailing market conditions. 30 to 80-day rate lock commitments are available. An early rate lock feature is available, allowing the borrower to lock the rate after preliminary underwriting. There is a 1% rate lock deposit payable at the time of rate lock, to be refunded at closing. Source

How long does it take to get a HUD 221(d)(4) loan approved?

The HUD 221(D)(4) loan process, from initial concept to final close, takes around 46 weeks on average. For a MAP one-stage application, the process will take about 5-7 months. For a MAP two-stage application, the process is more likely to take around 8-10 months.

For more information, please refer to this page and this page.